Explore the true loan in default meaning for student loans. This blog critiques how student loan defaults destroy careers, credit, and futures, questioning why the system punishes fresh graduates more than it helps them.

Introduction: The Student Debt Trap They Don’t Warn You About

They told you higher education unlocks opportunities. Universities painted glowing dreams, banks assured you support, and society said student loans are a “smart investment”. But here’s the bitter reality: when repayment begins, students quickly discover that these so-called opportunities can become lifelong burdens.

The criticism goes deeper when one examines loan in default meaning for student loans. Unlike credit card debt or consumer loans, student loan defaults carry even harsher, unforgiving consequences. And for young graduates, who are just stepping into unstable job markets, this becomes a trap disguised as “financial empowerment”.

This article does not sugarcoat. Instead, it pulls apart the illusions, exposes the biases of the system, and questions why the law treats struggling graduates as offenders rather than humans in transition.

Loan in Default Meaning for Student Loans: More Than a Definition

Technically, a student loan is considered “in default” when the borrower fails to make scheduled payments for a certain period. In the U.S., for example, missing 270 days of

payments (approximately nine months) puts federal student loans into default. In other countries, the timeframe can vary between 90 to 180 days.

In reality:

Default doesn’t mean recklessness. Graduates don’t deliberately ignore payments—they often cannot pay because of unemployment, underemployment, or crippling starting salaries in saturated job markets. Yet the system does not differentiate between inability and negligence. Both get thrown into the same damaging category: default.

So let’s be clear: the loan in default meaning for student loans is less about “missed payments” and more about an economic system that sets unrealistic expectations for the youngest members of the workforce.

The Brutal Credit Score Connection

When student loans slide into default, one of the first blows lands on the credit score. A default can send numbers plummeting by 100–200 points at once.

This isn’t just about numbers; it’s about lost opportunities. With a poor score: ● Graduates are denied credit cards or charged higher interest rates. ● Renting a home becomes difficult because landlords may check credit history.

● Even job offers may slip away in industries where background checks include credit reports.

Critics raise an obvious question: shouldn’t education be a tool for advancement, not a cause for long-term exclusion? Instead, loan defaults weaponize credit scores, chaining young graduates before they even step confidently into adulthood.

Timeline of a Student Loan Default: How Quickly It Spirals

The real tragedy lies in how student loan defaults escalate step by step:

● First Missed Payment (Day 1): Account goes delinquent. Late fees added. Borrowers often receive reminder messages.

● 30–90 Days Late: The loan status is reported to credit bureaus. Already, the credit score starts to sink.

● 90–180 Days Late: Delinquency intensifies. Debt collectors get involved. Borrowers start facing harassment calls.

● 270 Days (Federal Standards): Loan officially enters default. The entire unpaid balance becomes due. Benefits like flexible repayment plans vanish.

● After Default: Wages can be garnished, tax refunds can be seized, and government benefits withheld. Unlike other forms of debt, student loan defaults are rarely forgiven—even in bankruptcy.

This timeline exposes the cruelty. For a fresh graduate, nine months is barely enough time to adjust to post-college life. Yet, in the eyes of the system, it’s sufficient to brand them as “defaulters” for years.

Why the System is Heavily Flawed

Criticizing loan in default meaning for student loans becomes unavoidable once we acknowledge certain flaws:

1. No Room for Economic Reality

Student loans assume instant employability. But real-world jobs often pay less than promised or appear after frustrating delays. Why should laws refuse flexibility in such cases?

2. Unforgiving Credit Marks

Unlike other debts that may diminish in weight over time, student loan defaults cast long shadows. They remain on credit reports for up to seven years, if not more.

3. Limited Exit Strategies

Consumer debt can sometimes be discharged through bankruptcy. Student loans

often cannot. This makes them a debt for life.

4. Psychological Manipulation

The stigma of default is crafted as if it were a moral failure rather than a structural issue. Young borrowers shoulder shame, while policymakers continue to promote costly education models.

This unfairness reveals itself not just in economics but in morality. The younger generation, in pursuit of knowledge, becomes the scapegoat of a rigid repayment dogma.

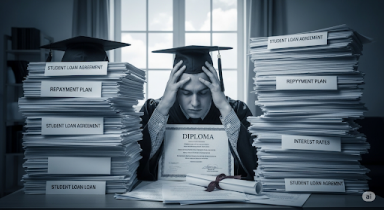

The Bigger Loss: Stalled Careers and Futures

The loan in default meaning for student loans does not stop at financial penalties. It interrupts personal progress:

● Career Choices Shrink: Graduates feel forced to accept any job, even poor-paying roles, just to avoid default.

● Entrepreneurship Suffers: Young innovators abandon dreams of startups because default means no access to credit.

● Mental Health Collapse: Anxiety, stress, and depression become natural outcomes of being crushed under unaffordable repayment schemes.

The result? Society loses bright minds to financial fear rather than gaining their full contribution.

Who Benefits From This Broken Cycle?

Criticism is not complete without asking the painful question who actually benefits from the student loan default trap?

● Banks and Loan Servicers: Interest, penalties, and collection fees ensure they profit even from defaults.

● Debt Collection Agencies: They thrive on borrowers’ desperation, often practicing borderline harassment.

● Governments: By securitizing student loans, they maintain economic leverage over graduates, treating education as revenue rather than empowerment.

Meanwhile, students supposedly the “future of the nation” carry lifelong debt records before they even start earning properly.

Comparing With Other Loans: The Harsh Truth

Why is it that student loan debt is treated more harshly than other forms of debt? ● Credit card debt? Can often be negotiated.

● Home loans? Forgiven or restructured in extreme crisis.

● Business loans? Corporations even receive bailouts.

But student loans? Almost never forgiven. This is especially ironic. The youngest borrowers, with the least experience, face the least forgiveness.

This disproportionality reeks of double standards. The law bends for corporations but not for students.

The Way Forward: What Needs Urgent Change

The system demands reform—not endless punishment. Here’s what critics argue must happen:

1. Grace Period Extensions

Students must be given longer adjustment windows after graduation before defaults are triggered.

2. Income-Based Repayment Must Be Universal

Repayment should adjust fairly to earnings. No graduate should default simply because their salary cannot meet the unrealistic EMI schedule.

3. Default Forgiveness Models

After demonstrated hardship, default status should be lifted. Financial recovery should be encouraged, not blocked.

4. Bankruptcy Protection Inclusion

Why should student loans be immune from bankruptcy discharge? This must change, making the law more balanced.

5. Regulating Harassment by Collectors

Strict, real-world consequences for recovery agents who cross ethical boundaries are necessary. Borrowers must be treated as humans, not prey.

A model built on fairness would empower students to recover, regenerate, and eventually contribute more productively to society.

Conclusion: Why We Must Criticize Student Loan Defaults

To conclude, the loan in default meaning for student loans reveals itself as more than a financial technicality. It is a deeply flawed system that punishes young people disproportionately. Student loan defaults strip graduates of dignity, destroy credit, and even rob society of innovation.

What should be a temporary hiccup is instead turned into a life sentence of economic punishment. This isn’t education empowerment; it’s education enslavement.

If governments and financial institutions really believe in the value of higher education, they must reform. They must build systems that rehabilitate, not imprison. Until then, each student loan default is not just an individual tragedy but a collective failure of society’s responsibility toward its future.